Solar Project Compliance IRS Audit: The 2026 Guide

Solar Project Compliance IRS Audit: The Complete Documentation Guide for Solar Installers (2026)

Why Solar Project Compliance IRS Audit Matters More in 2026

solar project compliance IRS audit has always been important. However, in 2026, the stakes are significantly higher. The One Big Beautiful Bill Act (OBBBA), signed on July 4, 2025, tightened Section 48E Investment Tax Credit (ITC) eligibility rules. As a result, the IRS is reviewing solar credit claims more carefully than ever before.

Analysts at Baker Botts noted in February 2026 that the IRS is treating some 2025 construction starts as potential “anti-circumvention” cases. That signals one thing clearly: your documentation needs to be bulletproof — before an audit letter ever arrives.

For solar installers and EPCs, poor documentation doesn’t just delay a credit. It can eliminate it entirely. Furthermore, it can damage your client relationships and your company’s reputation. The good news? Solid documentation is absolutely achievable. You just need to know exactly what to keep on file.

→ Learn more about our services and how they protect your projects from day one.

The Core Documents That Prove Solar ITC Compliance to the IRS

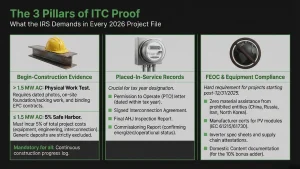

The IRS reviews several key areas during a solar ITC audit. Therefore, every project file should include these three documentation categories.

1. Begin-Construction Evidence

Under IRS Notice 2025-42, the rules for proving construction started changed significantly after the OBBBA. Here’s what applies now:

Physical Work Test — Required for all projects over 1.5 MW AC. You must show documented physical work of a significant nature. Acceptable evidence includes dated site photographs, on-site foundation or racking work, and binding EPC contracts with execution dates.

5% Safe Harbor — Only available for projects at or under 1.5 MW AC. You must pay or incur at least 5% of total project costs. Moreover, those costs must be specifically tied to the project — equipment purchases, engineering fees, or interconnection costs all qualify. Generic deposits do not.

Additionally, every project should maintain a construction progress log. This log creates a clear timeline that the IRS can follow from first activity through completion.

2. Placed-In-Service Records

The placed-in-service date determines which tax year the ITC applies to. It’s the most scrutinized date in any solar credit claim. Consequently, your file must include:

- Permission to Operate (PTO) letter — dated within the qualifying tax year

- Signed interconnection agreement — executed with the utility

- Final inspection report — issued by the AHJ with approval date

- Commissioning report — confirming the system is energized and operational

→ See how our permitting services help you lock in the right placed-in-service date every time.

3. Equipment and FEOC Compliance Documentation

Starting in 2026, Foreign Entity of Concern (FEOC) compliance is a hard eligibility requirement for Section 48E credits. The OBBBA extended FEOC restrictions to major clean energy tax credits, including solar ITC. Projects that began construction after December 31, 2025 must therefore confirm they received no material assistance from Prohibited Foreign Entities — including entities controlled by China, Russia, Iran, or North Korea.

Your equipment file should include:

- Manufacturer certifications for PV modules (IEC 61215/IEC 61730 standards)

- Inverter spec sheets and compliance certificates

- FEOC attestation letters or supply chain declarations from equipment vendors

- Domestic Content documentation, if you’re claiming the 10% bonus credit adder

For more context, review the SEIA Commence Construction Guidance and IRS Notice 2026-15 on material assistance rules.

How PE-Stamped Plans Strengthen Solar Project Compliance at Audit

A PE-stamped plan set does more than satisfy your AHJ. In an IRS audit, it functions as independent third-party verification that your project was real, legitimate, and code-compliant.

Think about what an auditor is really asking: Did this project actually happen? Was it built properly? A PE-stamped engineering package — signed by a licensed Professional Engineer — answers both questions directly.

Specifically, it confirms:

- The system was professionally designed to NEC 2023/2026 standards

- Structural and electrical loads were calculated by a licensed engineer

- Equipment was correctly specified for the actual site

- The project met all local AHJ requirements

Projects without proper engineering documentation face a much higher risk of IRS follow-up, credit disallowance, and financial penalties. By contrast, projects with a complete engineering file typically resolve audits quickly and cleanly.

→ Get PE-stamped plan sets in as little as 24 hours — all 50 states, 99% AHJ approval rate.

Your 6-Step Audit-Ready Documentation Checklist

Staying compliant doesn’t require extra time — it requires the right system. Follow this sequence on every project:

- Project Initiation — Date and execute all contracts, EPC agreements, and equipment purchase orders. Photograph the site before, during, and after construction.

- Engineering Phase — Secure PE-stamped structural and electrical plan sets before breaking ground. Reference actual equipment models in the drawings.

- Permitting & Inspection — Retain all AHJ-issued permits, inspection cards, and approval notices. These connect your engineering records to official government documentation.

- Interconnection & PTO — Save the signed interconnection agreement and PTO letter. The IRS uses these as primary proof of placed-in-service date.

- FEOC & Equipment Compliance — Collect manufacturer certificates and supply chain attestations before project closeout — not after an audit notice arrives.

- Tax Year Close — Compile a complete project binder organized by IRS Form 3468 line items. Your client’s tax professional can then access everything they need instantly.

The IRS generally has three years to audit a return. However, FEOC compliance items fall under Section 50 recapture rules with a 10-year window. Therefore, maintain your documentation accordingly.

The July 4, 2026 Deadline: Act Before the Window Closes

Time is the most critical factor in solar project compliance for IRS audits right now. Under the OBBBA, solar projects must begin construction by July 4, 2026, and be placed in service by December 31, 2027, to qualify for the full 30% Section 48E ITC.

For large projects over 1.5 MW AC, physical construction must be underway before that date. For smaller projects, the 5% cost incurrence standard still applies. Either way, the documentation you generate this spring becomes the foundation of every future ITC claim.

Don’t wait for permitting delays or supply chain issues to eat into your window. Start your engineering, execute your contracts, and build your documentation stack now.

Protect Your Clients from IRS Audit — Start With the Right Engineering Partner

EnergyScape Renewables delivers PE-stamped plan sets in as little as 24 hours, across all 50 states, with a 99% AHJ approval rate. When an IRS auditor reviews your project, your engineering package needs to be complete, accurate, and professionally stamped.

👉 Get PE-Stamped Plans: energyscaperenewables.com

Sunscape Solar gives you the project management and documentation tools to track every permit, milestone, and compliance checkpoint — all in one platform. Built specifically for US solar installers and EPCs.

👉 Explore Sunscape Solar: sunscape.solar

Frequently Asked Questions — Solar Project Compliance IRS Audit

Q: What documents do solar installers need for an IRS tax credit audit? A: Solar installers need begin-construction evidence (dated site photos, contracts), placed-in-service records (PTO letter, interconnection agreement, commissioning report), manufacturer certifications, and FEOC compliance attestations for Section 48E projects.

Q: Does a PE-stamped plan set help with IRS audit compliance? A: Yes. A PE-stamped plan set confirms the project was professionally engineered, code-compliant, and tied to actual equipment — providing strong third-party proof of legitimacy during an IRS review.

Q: What is the 5% Safe Harbor for solar ITC in 2026? A: Under IRS Notice 2025-42, the 5% Safe Harbor is only available for solar projects at or under 1.5 MW AC. Projects must incur at least 5% of total qualifying costs. Projects over 1.5 MW must use the Physical Work Test instead.

Q: What is the solar ITC construction deadline in 2026? A: Solar projects must begin construction by July 4, 2026, and be placed in service by December 31, 2027, to qualify for the full 30% Section 48E Investment Tax Credit under the OBBBA.

Q: What is FEOC compliance for solar tax credits? A: FEOC (Foreign Entity of Concern) compliance means confirming your solar equipment received no material assistance from entities controlled by China, Russia, Iran, or North Korea. It’s a hard eligibility requirement for Section 48E credits on projects beginning construction after December 31, 2025.

sjayakanth@energyscaperenewables.com